TL;DR:

- Dental insurance networks influence costs, provider choices, and access to preventive or specialty care.

- Choosing in-network providers significantly reduces out-of-pocket expenses for common dental procedures.

- Families should verify network participation annually and consider combining insurance with membership plans for affordability.

Choosing a dental plan for your family feels straightforward until you realize the network your dentist belongs to can change everything about your costs and access to care. Many families in San Bernardino and the Inland Empire sign up for Denti-Cal, HMO, or PPO plans without fully understanding how dental insurance networks shape their experience. The result? Surprise bills, limited provider choices, and missed savings that could have stayed in your pocket. Understanding how these networks work is one of the most proactive steps you can take for your family’s oral health and your monthly budget.

Table of Contents

- What is a dental insurance network and why do they exist?

- How dental networks impact coverage, costs, and provider choice

- The special case for Denti-Cal and HMO plans: What families often miss

- Comparing dental insurance networks with alternative affordable care options

- Making the most of your dental insurance network: Practical steps for San Bernardino families

- Our perspective: What most families overlook about dental insurance networks

- Affordable, high-quality dental care options in San Bernardino

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| In-network means savings | Dentists in your insurance network offer lower prices thanks to negotiated rates. |

| Confirm network status | Always verify your dentist is in-network before booking to avoid surprise costs. |

| Know your plan’s limits | Denti-Cal and HMO plans restrict provider choice, so check rules before committing. |

| Alternatives exist | Membership programs and uninsured options may offer affordable care if you lack traditional coverage. |

What is a dental insurance network and why do they exist?

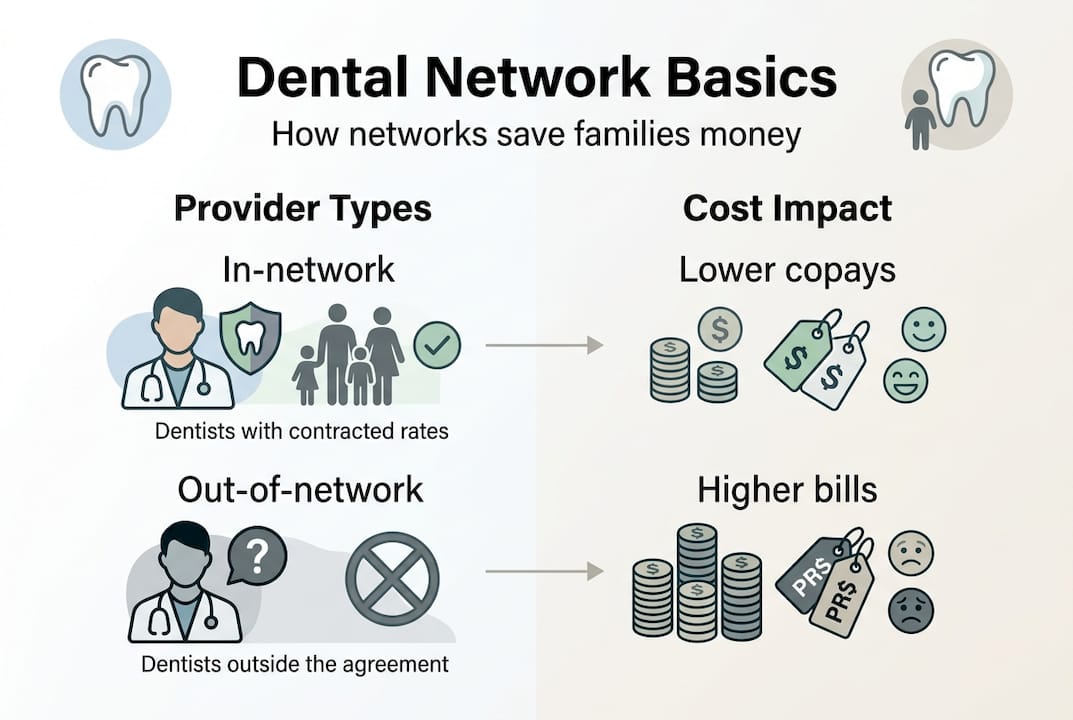

A dental insurance network is a group of dentists and dental practices that have signed contracts with a specific insurance company. These contracts set agreed-upon rates for dental procedures, which is how insurance companies keep costs manageable for their members. Think of it like a preferred pricing arrangement: the dentist agrees to charge less for covered services, and in return, the insurance company sends patients their way.

The core purpose of a network is cost management. Dental networks negotiate rates with providers to keep member costs low, which benefits both the insurer and the patient. Without these negotiated rates, a routine cleaning or filling could cost significantly more out of pocket.

Here is the key distinction families need to understand:

| Provider type | What it means | Cost impact |

|---|---|---|

| In-network | Contracted with your insurer | Lower copays, predictable costs |

| Out-of-network | No contract with your insurer | Higher costs, possible balance billing |

Not every dentist joins every network. Some practices choose to remain out-of-network because the reimbursement rates set by insurers are too low to cover their operating costs. Others specialize in services that certain networks do not adequately reimburse. This is not a red flag about a dentist’s quality. It simply means your coverage may work differently with them.

Common misunderstandings families have include:

- Believing that any licensed dentist automatically accepts their plan

- Assuming that out-of-network always means no coverage at all

- Thinking that all plans within the same insurer share the same network

- Confusing plan type (HMO vs. PPO) with network participation

Understanding dental insurance terms before you book an appointment saves you from these costly surprises. A few minutes of research up front can protect your family from hundreds of dollars in unexpected charges.

How dental networks impact coverage, costs, and provider choice

Now that you know what networks are, see how choosing the right one impacts everything from your wallet to who treats your child’s cavities.

The financial difference between in-network and out-of-network care is real and measurable. Choosing an in-network provider can reduce your costs significantly compared to going out-of-network. Here is a practical look at how this plays out for common procedures:

| Procedure | In-network cost (est.) | Out-of-network cost (est.) |

|---|---|---|

| Routine cleaning | $0 to $20 copay | $80 to $150 |

| Dental X-rays | $0 to $15 copay | $50 to $100 |

| Tooth filling | $20 to $50 copay | $150 to $300 |

| Crown | $150 to $300 copay | $800 to $1,500 |

These numbers illustrate why network status matters so much for families managing tight budgets. For Denti-Cal and HMO members, the stakes are even higher because these plans often require you to stay within a specific network or face full out-of-pocket costs.

Preventive care is where in-network benefits shine brightest. Most plans cover two cleanings and annual X-rays at little or no cost when you visit an in-network provider. The benefits of regular checkups go far beyond clean teeth. Catching a small cavity early costs far less than treating an infected tooth later.

Here is what network participation affects for your family:

- Which dentists and specialists you can see at reduced cost

- Whether referrals are required for specialty care

- How much your insurance pays versus what you owe

- Whether your plan covers care received outside the network at all

Pro Tip: Before scheduling any appointment, call both your insurance plan and the dental office to confirm current network participation. Networks change, and a provider who was in-network last year may not be today. Always verify, even if you have visited the same office before.

To maximize dental insurance value, prioritize in-network preventive visits and plan any elective procedures within the same benefit year to make the most of your annual maximum.

The special case for Denti-Cal and HMO plans: What families often miss

Families with Denti-Cal or HMO coverage face special rules. Let’s break down what this means for you.

Denti-Cal and HMO plans often have stricter network requirements that directly affect what providers you can see. Unlike PPO plans that give you more flexibility to go out-of-network (with higher costs), HMO and Denti-Cal plans typically require you to choose a primary dental provider and stay within that specific network for all covered services.

Here is how to find an in-network dentist in San Bernardino step by step:

- Log into your insurance plan’s website and use the provider search tool

- Filter by your city or zip code to find local options

- Call the dental office directly to confirm they are currently accepting your specific plan

- Ask whether they accept new patients and have availability for your family

- Confirm which services are covered under your plan before your first visit

Families who skip step three often find out at the front desk that the provider listed online is no longer accepting their plan. This is a frustrating and avoidable situation.

Common pitfalls with Denti-Cal and HMO plans include:

- Seeing a specialist without a required referral from your primary dentist

- Visiting a provider who is listed in the directory but is no longer contracted

- Missing annual enrollment windows to change your primary dental provider

- Assuming emergency care is always covered outside your network

Pro Tip: If your preferred dentist is not in your plan’s network, ask them whether they plan to join or whether they offer a sliding scale or membership program for patients with limited coverage. Some practices, including those choosing a dentist resources recommend, offer affordable alternatives for patients in exactly this situation.

For families using best dental insurance plans like Denti-Cal, understanding these network rules is the difference between getting care and going without it.

Comparing dental insurance networks with alternative affordable care options

But what about families without insurance? Let’s compare how dental networks stack up against alternatives in San Bernardino.

Dental membership programs offer simplicity and predictable costs, but may lack emergency or specialty coverage you would get with insurance. This trade-off is worth understanding before you decide what is right for your family.

| Feature | Insurance network | Dental membership plan |

|---|---|---|

| Monthly cost | Varies (often $20 to $80+) | Often $20 to $50 per month |

| Waiting periods | Common for major work | Usually none |

| Network restrictions | Yes, provider must be contracted | Limited to participating offices |

| Emergency coverage | Often included | May be limited |

| Specialist access | Covered with referral | Varies by program |

| Qualifying requirements | Income or employer-based | Open enrollment, no approval |

Here is when a membership plans for uninsured families may be the better fit:

- You do not qualify for Denti-Cal and your employer does not offer dental benefits

- You want immediate access to care without waiting periods

- Your dental needs are primarily preventive and routine

- You prefer a flat, predictable monthly cost over variable copays

- You want flexibility to choose your provider without network restrictions

Many families in the Inland Empire use both strategies. They may carry a basic insurance plan for major coverage while also enrolling in a membership program for routine care at a specific practice they trust. This layered approach can be surprisingly cost-effective when you run the numbers.

Making the most of your dental insurance network: Practical steps for San Bernardino families

Whichever path you choose, here is how to get the most value out of your network benefits.

Following a checklist helps ensure you do not miss critical steps that can save you hundreds per year on dental care. Here is a practical guide designed for Inland Empire families:

- Verify your network: Confirm your dentist is in-network at the start of each year, not just when you first enroll

- Schedule preventive visits early: Book your two annual cleanings in January and July to spread benefits evenly

- Understand your annual maximum: Most plans cap benefits at $1,000 to $2,000 per year. Plan major work accordingly

- Request pre-authorization: For crowns, implants, or orthodontics, ask your dentist to submit a pre-approval request before treatment begins

- Coordinate benefits if you have two plans: If your child is covered under both parents’ plans, coordinate to reduce out-of-pocket costs significantly

- Appeal denied claims: If a claim is denied, request an explanation of benefits and ask your dentist’s office to help you file an appeal

- Review your dental insurance checklist annually: Coverage rules, networks, and your family’s needs all change over time

Pro Tip: When a claim is denied, do not assume the decision is final. Many denials are overturned on appeal, especially when your dentist provides supporting documentation showing the treatment was medically necessary. Your dental office’s billing team is your best ally in this process.

Staying organized and proactive with your coverage is not just about saving money. It is about making sure your family gets the care they need, when they need it, without unnecessary stress.

Our perspective: What most families overlook about dental insurance networks

After years of working with San Bernardino families, we have noticed a pattern. Most people accept whatever dental plan their employer or the government assigns them, glance at the card, and assume everything is covered. The network question never comes up until there is a problem.

What we have learned is that a thoughtful network decision made once a year, during open enrollment or when your plan renews, can set the foundation for years of affordable, consistent care. It is not just about the lowest premium. It is about whether the dentist you trust is in your network, whether specialty care is accessible, and whether your family can get seen quickly when something goes wrong.

The unexpected payoff of getting this right is continuity of care. When your family sees the same trusted provider year after year, that dentist knows your history, catches changes early, and builds a relationship that makes every visit less stressful. Affordable membership plans can support this continuity for families who are between insurance plans or who simply want more flexibility. We encourage every family to evaluate their options each year, look beyond just the monthly cost, and ask the question that matters most: does this plan actually connect me to the care my family needs?

Affordable, high-quality dental care options in San Bernardino

At Monteluz Dental Specialty Group, we believe that understanding your insurance network should open doors, not close them. We accept Denti-Cal, PPO, and HMO plans, and we also offer affordable dental membership plans starting at just $20 per month for families without insurance coverage.

Whether your family needs routine preventive care, dental implant solutions, or orthodontic care, our bilingual team is here to help you navigate your coverage and get the care you deserve. Call us or visit our website to ask about your specific plan and find out how we can make quality dental care work for your family’s budget and schedule.

Frequently asked questions

What is the main benefit of choosing an in-network dentist?

In-network providers give you negotiated, lower rates on care, which means smaller copays and fewer surprise bills compared to seeing an out-of-network dentist.

How can I find out if my San Bernardino dentist is in-network?

Checking network participation before booking is essential for maximizing insurance benefits. Call your dental plan’s member services line and the dental office directly to confirm their current contract status.

Are dental membership plans better than insurance networks for uninsured families?

Dental membership programs are cost-efficient but have different coverage scopes. They work well for routine and preventive care but may not cover emergencies or specialist services the way traditional insurance does.

Can I use both Denti-Cal and private dental insurance together?

Coordinating dental benefits requires careful review of your coverage rules, but some families can combine plans to reduce out-of-pocket costs. Always confirm eligibility and provider participation with both plans before scheduling care.

Recommended

- Affordable Dental Care Workflow for Families Near You

- Why Dental Insurance Matters for San Bernardino Families

- Affordable Dental Care – Impact on Family Well-being

- Dental Insurance Terms Explained for Families